A dollar today is worth more than a dollar tomorrow.

An initial lump-sum investment of \(P\) dollars into an account

that earns an annual interest rate of \(k\) compounded continuously

its future value (FV) \(P(t)\)

after \(t\) years will be \(S = P\mathrm{e}^{kt}.\)

Conversely, given a future value \(S\) having been invested at an annual interest rate of \(k\)

compounded continuously for \(t\) years, its present value (PV) \(P\) must be

\(P = S\mathrm{e}^{-kt}.\)

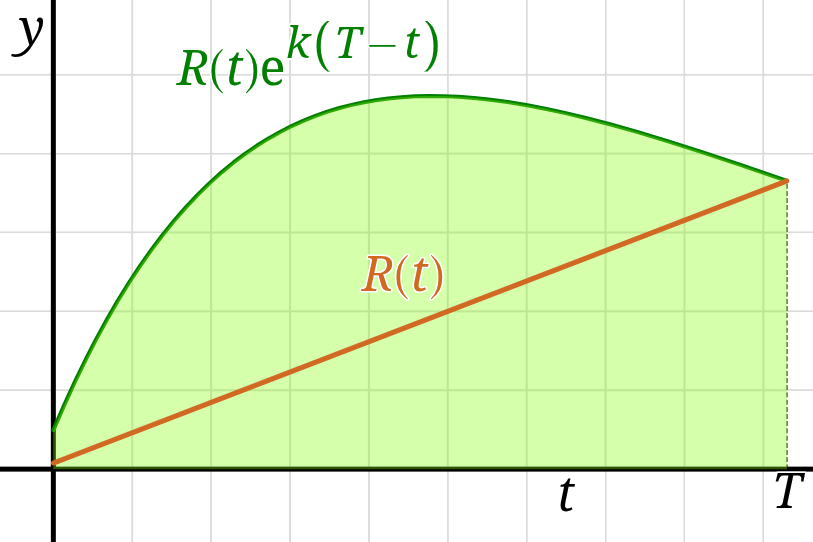

For a continuous cash flow (income stream) of \(R(t)\) dollars-per-year,

the accumulated future value of \(R(t)\) after \(T\) years

is given by the integral

\[ \int\limits_0^T R(t) \mathrm{e}^{k(T-t)}\,\mathrm{d}t

{\color{gray} \quad = \quad

\mathrm{e}^{kT}\int\limits_0^T R(t) \mathrm{e}^{-kt}\,\mathrm{d}t\,. }\]

Conversely the present value of a continuous cash flow of \(R(t)\) dollars-per-year

after \(T\) years is given by the integral

\[ \int\limits_0^T R(t) \mathrm{e}^{-kt}\,\mathrm{d}t\,. \]

For a continuous cash flow (income stream) of \(R(t)\) dollars-per-year,

the accumulated future value of \(R(t)\) after \(T\) years

is given by the integral

\[ \int\limits_0^T R(t) \mathrm{e}^{k(T-t)}\,\mathrm{d}t

{\color{gray} \quad = \quad

\mathrm{e}^{kT}\int\limits_0^T R(t) \mathrm{e}^{-kt}\,\mathrm{d}t\,. }\]

Conversely the present value of a continuous cash flow of \(R(t)\) dollars-per-year

after \(T\) years is given by the integral

\[ \int\limits_0^T R(t) \mathrm{e}^{-kt}\,\mathrm{d}t\,. \]

These integrals reduce to the familiar formulas for continuously compounded annuities, when \(P\) dollars are deposited \(n\) times per year, and when cash flow function is constant: \(R(t) = nP.\)